One of the strangest oddities in Islam is that Islam bans interest, both receiving and paying it. Prophet Muhammad probably took this rule from Judaism and continued it in Islam. He may have seen some harms caused by interest and decided to ban it outright, or maybe he wanted to add more credence and legitimacy to his religion by taking laws from Judaism. Either way, banning interest has led to many Muslims suffering and struggling their entire lives, living in mediocrity rather than excelling and building capital for their families. I am arguing here that Islam is bad for humanity, and in particular, this rule of forbidding interest is bad for humanity and harms Muslims that follow it. I will give actual financial numbers to show that interest actually can be beneficial, especially when it comes to renting vs. owning.

What is Riba?

Riba is defined to be of many parts, and one part of riba is interest. This is because Prophet Muhammad said:

“The Messenger of Allah said: ‘Gold for gold, weight for weight, like for like; and silver for silver, weight for weight, like for like. Whoever gives more or takes more has engaged in Riba.”‘ (Nasai 4569)

So based on this statement and others, Sunni Muslims are forever never allowed to charge interest or pay interest. It also puts other limitations on them such as trading gold for gold on the spot, which will not be discussed here.

Punishment for riba

Riba is considered extremely bad, so bad that it deserves Allah’s wrath and Muhammad’s cursing:

The Prophet (ﷺ) cursed the lady who practices tattooing and the one who gets herself tattooed, and one who eats (takes) Riba’ (usury) and the one who gives it. And he prohibited taking the price of a dog, and the money earned by prostitution, and cursed the makers of pictures. (Bukhari 5347)

The disbelievers at the time of Muhammad used to say that riba and trade were the same. The Quran doesn’t explain why they are different but rather just states that they are different:

Those who consume interest cannot stand [on the Day of Resurrection] except as one stands who is being beaten by Satan into insanity. That is because they say, “Trade is [just] like interest.” But Allah has permitted trade and has forbidden interest. So whoever has received an admonition from his Lord and desists may have what is past, and his affair rests with Allah . But whoever returns to [dealing in interest or usury] – those are the companions of the Fire; they will abide eternally therein. (Quran 2:275)

There is so much emphasis put on how terrible riba is, that it’s worse than having illegal sexual intercourse, that you will be told to fight with Allah on the day of judgment, that it’s cursed, and so on. Essentially, you are doomed if you partake in it. You should avoid it whenever and however possible. Most practicing Muslims avoid interest like the plague

But riba is not interest!

Riba is not interest. That is correct. Riba is a bigger category and contains many different things, one of which is interest. Interest is categorically a form of riba. There is no way around it. When you trade money for money of unequal amounts without a product involved, you are involved in riba. There is a plethora of evidence online ad naseum that interest is riba is so I will not spend any more time proving it here.

Is interest bad?

Yes and no. There are some forms of interest which are harmful. Excessive interest can be very harmful to individuals and society. Examples of this are short-term cash loans lent out by companies like CashMoney which can be as high as 30-80% (if you calculate it), as well as credit card interest rates (19-23%), department store cards (30%), as well as those rent-to-own furniture stores tend to be a rip off. I am in favor of putting limitations on interest, but not banning it outright.

Sometimes societies are harmed by loans which bankrupt them and they can never pay them back. There are definitely some limitations that can be placed on loans in order for society to thrive.

There are also many ways interest benefits a society, and I will describe one example here.

Why forbidding interest is bad for Muslims

In today’s modern world, interest being forbidden puts you at a huge disadvantage. This is what I experienced as a Muslim. I felt that the risk of getting Allah’s displeasure was too great to involve myself in riba, so we rented. We could not find a way to buy a home without involving ourselves in riba, so I continued to rent. We had a big family, there was my wife, my growing family of 5 kids living in rent. It’s worth the struggle to avoid Allah’s wrath!

But.. Islamic finance?

There are Islamic alternatives to interest based mortgages. The issue is that there is no need for such workarounds when the interest based model works perfectly fine in this case, as demonstrated in this article. Why use complicated workarounds for a system that isn’t broken? As a Muslim, I wrote an review on a company called Ansar Housing which offered Islamic based mortgages. You can read it at the end of this blog post. It is out of the scope of this article to discuss all the alternatives. The crux of this post is that the conventional system works well, and there’s no need for the rigidity of Islamic finance.

Difficulties renting

When we started renting back in 2006, the rent was around $1250 a month for a 1 bedroom. By the time 2015 came, I had to pay around $1650 a month of rent for a small townhouse (less than 1500 square feet) and could not even find a suitable place to rent for my family at this price when my landlord said we had to leave because he wanted to sell it. I was worried that I may have to pay around $2000+ a month as my family had grown and the places we looked at were not sufficient. This would be $24,000 Canadian Dollars a year completely burned by renting. Not to mention we had several issues with renting because we had a big family and nobody wants to rent to a large family. There was also the stress of having to not knowing how long you would be able to stay

Did you leave Islam because of not having a mortgage?

No, of course not. I left Islam because I found the Quran to be false. Once I realized this, there was no issue in getting a mortgage. I would have gladly bore the difficulties of living without a mortgage if I had to because I wanted Allah’s pleasure and Jannah in return. Of course, if it’s all a lie, then Muslims are wasting their lives sacrificing for nothing.

The blessing of leaving Islam

When I finally realized Islam was false, I decided to buy a house on riba. Here is how the math worked out. We bought a beautiful 4 bedroom 2500 square foot home and my family couldn’t be happier!

Is a mortgage bad for the bank?

Is the mortgage bad for the bank? My mortgage interest rate is 2.5%. This is REALLY cheap, so how can the bank afford to loan the money at such a low price? Simple!

- The bank has access to cheap money, your bank deposits and other money that people trust them with such as GICs.

- Your down payment is held

- Your property is valued and they have a lien on it so they can sell it if you don’t pay.

In essence, the bank has very little risk and can give this win-win situation. They have low risk and you get cheap money. There is nobody losing here, it’s a mutually beneficial deal. Banks are happy and buyers are happy.

I will explain how a 2.5% interest ends up making it almost guaranteed cheaper than renting, especially in the long run.

So if riba is cursed, I have to ask, why? Who is losing here? Who is being harmed here? Who is suffering? In fact, nobody is being harmed, this is a really good setup, and it works well. Islam was made by a man who did not predict the way the world finance would evolve, and he did not realize that interest was not something that should be banned.

The math on renting vs. owning

Here’s the math. Over time, you save tons of money by owning. For a $650,000 home over 25 years, with the 5% down ($40,000) here is how it works out for the first month. See the attached excel sheet or visit RBC Mortgage Calculator for an interactive example

| # | Principal Outstanding | Principal & Interest Payment | Interest | Principal |

|---|---|---|---|---|

|

1

|

$634,400.00

|

$2,841.90

|

$1,314.84

|

$1,527.06

|

So what this means is you will have to pay $2841 (significantly more than rent), but the interest is only $1300. The $1527 principal is yours to keep when you sell the home. It’s a sort of forced savings that you get back eventually!

Now keep in mind, that even when I was paying $1650 in rent, I only had a small home that we barely fit in and hardly room to park our cars.

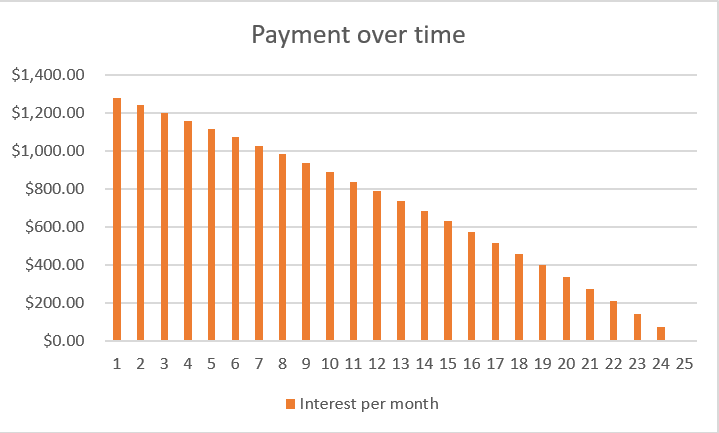

Monthly reduction in cost over time for buying

Let’s see how this interest payment reduces over time.

| End of Year | Interest/month |

| 1 | $1,279.66 |

| 5 | $1,116.43 |

| 10 | $888.20 |

| 15 | $629.78 |

| 20 | $337.18 |

| 25 | $5.88 |

Compare this to how my rent was actually INCREASING every year from 2006 to 2016! In year 5, I am actually only paying $1100 a month for the actual house!

By the way, the total cost of ownership is a bit more, because you have to factor in property tax, maintenance, and hydro (which sometimes you pay even when you rent). For me, this is about $500 a month.

Paying off the capital

The mortgage is a sort of forced savings. Since December 2016 I have paid off over $70,000 off my mortgage on top of the interest. This is insane compared to when I was renting I had nothing. This is all money that I will get back when I sell.

Increase in home value

Over the last 2 years, my home has increased approximately $200,000 in value. Yes, that’s right. If I sold the home now, I would have over $100,000 in profit that I could use for my kids’ education, travel if I so wished, and so on.

In summary buying a home…

As you can see, even from the start I am not only paying the same amount to my rent ($1300 interest plus $500 in other costs) but I get

- Much nicer house – bigger and better and room for my family that they are happy in

- PEACE OF MIND – Not having to worry about landlord selling or having to move

- No landlord can bother me about having kids issues such as writing on the walls etc.. If the kids damage it, I have to fix it myself.

- I can make renovations in the home if I so choose (I actually opted to get solar panels on my home which earns me $4k a year)

- It saves me money over time due to reduction in remaining mortgage

- It grows in value over time

I wish all Muslims well and to consider the points above as an indication that Islam is a man-made system that is flawed, and that Muslims would do better to leave Islam and to live happy lives without any religious influence. My life has improved drastically after leaving Islam and I wish you also the same!

Appendix:

Brother why don’t you read and understand full verses of interest rather than quoting out of context … only consuming interest is forbidden in Islam, if you read Quran it only talks about consuming interest as Haram and that is Mercy from Allah on people who can’t afford to pay back, look at below verses how merciful is Allah he is asking people to Leave the Remains of interest and also give time until they can pay back. Hadiths was only for that time based on situations but its not a Rule for all times….The book of rules is Quran. Please show me a verse where it shows giving interest is Forbidden can you…offcourse you can’t, all your queries and information Lack knowledge you left Islam before understanding it fully, I also have doubt but will i leave my Family if I have doubt on them…then how can I leave Allah i will understand Islam in the light of Quran not on Historical records

2.278

O you who have believed, fear Allah and give up what remains [due to you] of interest, if you should be believers.

2.280

And if someone is in hardship, then [let there be] postponement until [a time of] ease. But if you give [from your right as] charity, then it is better for you, if you only knew.

4.161

And their taking usury though indeed they were forbidden.

Please read these and other verses in Quran in context and understand.

Great article. Many wise words, as usual. Showing the fatal flaws in Islam. Flaws that brainwashed Muslims will, of course, attack but have no real comeback against. Thank you.

http://www.reformingislam.org

You make a very clear case on rent vs. mortgage, and why non-extortion levels of interest make a lot of sense. I’ve been looking for an example (numerical breakdown) contrasting a ‘halal’ mortgage versus a conventional western mortgage. I suspect that in the Islamic financing world, it’s really just interest by another name, when you look at all the inflows and outflows. However, I would like to demonstrate that with numbers (or have my suppositions challenged).

LOL commenter Firasath is like: Dude you’re wrong, read it right . you left Islam before understanding it fully, As if that was the only issue with Islam.

As for me its nice to try and understand this Riba stuff. As a non-Muslim I was trying to understand it an failed. It just makes no sense as interest is just the reward of lending money. Its basically profit.

I tried Youtube but all the videos seem to be about why Riba is bad. Maybe you should make a Youtube video showing how its not nearly as bad?

I found the narrative of this article was to ridicule and provoke Islam rather then explain interest in great detail. I see you have cherry picked facts and skewed statistics. You pulled statements from hadiths which were weak, also from the Quran that you pulled is out of context without finishing the latter verses. But your math is actually inaccurate because $650,000 at 5% for 25years is roughly $1,625,000! Well over a million and a half bucks for a 25year period. Where as renting $1650/month for 25 years is only $495,000! So renting is much better in the long run because you will pay 3x less! Here’s the math to prove it:

$1,650 X 12 month= $19,800

$19,800 X 25 years= $495,000

As you can see the math here doesn’t lie, neither is it misleading to the masses nor is it biased.

Also housing bubbles are imminent, more and more recessions are among us. Which tremendously bring your $650,000 house down by 40% easily. Which means over time it will not gain value, it will loose value! Which bring that value of the house down to: $390,000

$650,000 X 0.40= $260,000

$650,000 – $260,000= $390,000✅

Every 8-10 years prices of houses will either adjust themselves or banks can continue to lend, this causing more bubbles and extreme recessions leading disastrous economical impact on the world and people losing their life hard work in retirement for the scheme known as interest. Mainly because lending institutions don’t create wealth or money, rather they create debt which is injected into our economy to the point of bursting!

You said:

> But your math is actually inaccurate because $650,000 at 5% for 25years is roughly $1,625,000! Well over a million and a half bucks for a 25year period.

This is totally incorrect.

Firstly, nobody pays 5% interest nowadays. My current interest rate is around 2.5% and I will be renewing around 3.5%.

Second of all, your math is awful! How did you get $1,625,000?

650,000*.05= 32500

32500*12 = $812,500

Why did you double it?

Thirdly, your math is awful! The interest amount doesnt stay the same over 25 years dummy. It decreases every year. Run a mortgage calculator and see the declining balance sheet. I even did the homework for you and attached an excel file you can play around with: http://abdullahsameer.com/blog/wp-content/uploads/2017/12/Mortgage-Calculator.xlsx

As for house prices dropping, yeah it does happen sometimes. That’s the one thing you got right. But even since the huge 2008 crash, prices have recovered in America:

https://tradingeconomics.com/united-states/housing-index

Those who bought in the crash would have been the best off now!